China factory output stalls — while America surges

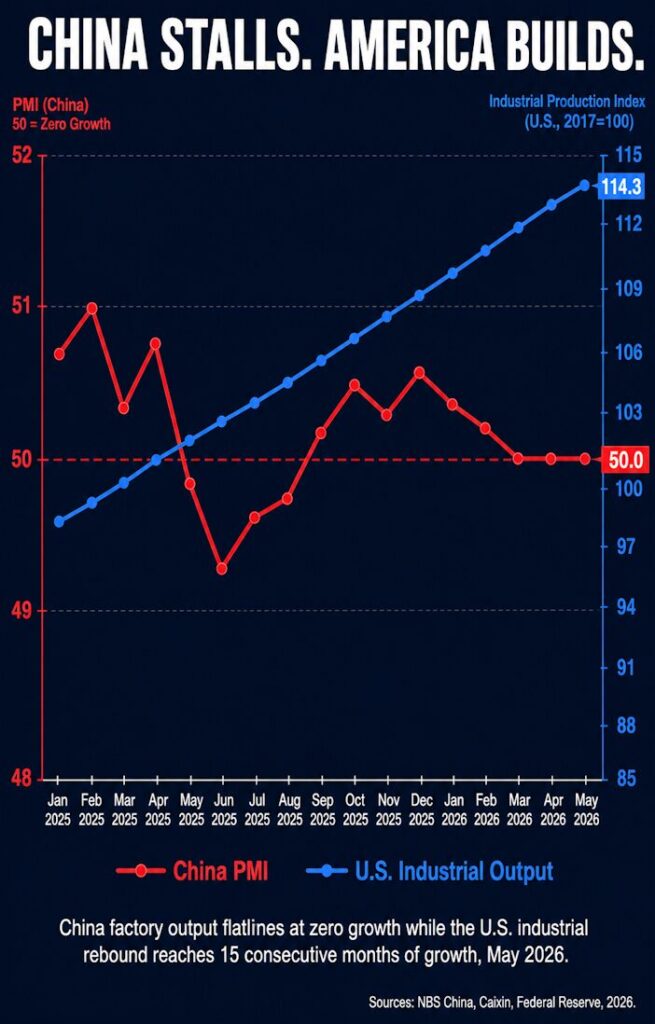

China factory output flatlined in May 2026. The official National Bureau of Statistics PMI hit exactly 50.0 — the precise zero-growth line between expansion and contraction.

That number sounds neutral until you understand what it means in context.

China’s manufacturing engine, the largest in the world by volume, is producing at a pace that generates no net growth whatsoever.

The private Caixin PMI, which tracks smaller export-oriented firms more closely, fell even harder — dropping to 48.3, its lowest reading since September 2022 and its first contraction in eight months.

Export orders fell to 48.6 in May from 50.3 in April. Factories are still producing. But fewer buyers are showing up.

The energy shock from the Iran war and the Strait of Hormuz blockade is hitting Chinese manufacturers brutally.

Raw material input costs rose at their fastest pace since March 2022.

The manufacturing input price index hit 60.5 in May — well above the 50 expansion line — meaning costs are rising even as revenues stagnate.

Supplier delivery times lengthened to their greatest extent since December 2022.

Petrochemical and upstream industries are being squeezed hardest by imported producer price inflation.

Beijing built its industrial dominance on two pillars: cheap energy and cheap labor. Both are eroding.

Chinese manufacturing wages have risen steadily for over a decade. The era of dirt-cheap Chinese factory output is not what it once was — and the Iran war energy shock is now accelerating that structural pressure faster than Beijing’s planners expected.

Germany contracts, Europe struggles — the Iran war energy toll

Germany, Europe’s industrial engine, is not faring much better. German industrial production fell 0.7% in March 2026, sitting 2.8% below the same month the previous year.

Overall German industrial production remains close to a post-pandemic low, and structural headwinds will keep output subdued regardless of how the Iran war evolves.

The picture across sectors is mixed — computer equipment and optical products grew 5.0% while mechanical engineering fell 2.7% and metal products dropped 2.4%.

Europe’s broader manufacturing outlook is darkening too.

Capital Economics warned that the eurozone economy might contract in Q2 2026, with consumer confidence dropping sharply since the Iran war began.

Europe imports heavily from the Persian Gulf energy corridor. Every week the Strait of Hormuz remains contested is another week of elevated energy costs bleeding European factory margins.

To be fair to the facts, Europe’s energy vulnerability did not begin with the Iran war. It was self-inflicted over two decades of ideologically driven energy policy.

European governments — led by Germany — systematically dismantled nuclear power capacity, rejected domestic fossil fuel development, and built their industrial energy model around the assumption that cheap Russian gas and Middle Eastern oil would always flow uninterrupted.

Green energy mandates accelerated the process. Wind and solar cannot power steel mills and chemical plants at the scale European industry requires.

When the energy corridor tightens, European factories have nowhere to turn — because their own governments spent twenty years eliminating the alternatives.

The Iran war exposed that vulnerability. It did not create it.

Thus, now Brussels is simultaneously trying to reduce dependence on Chinese goods while absorbing an energy shock it has no short-term answer for.

The result is an industrial sector caught between two pressures with relief in sight for neither.

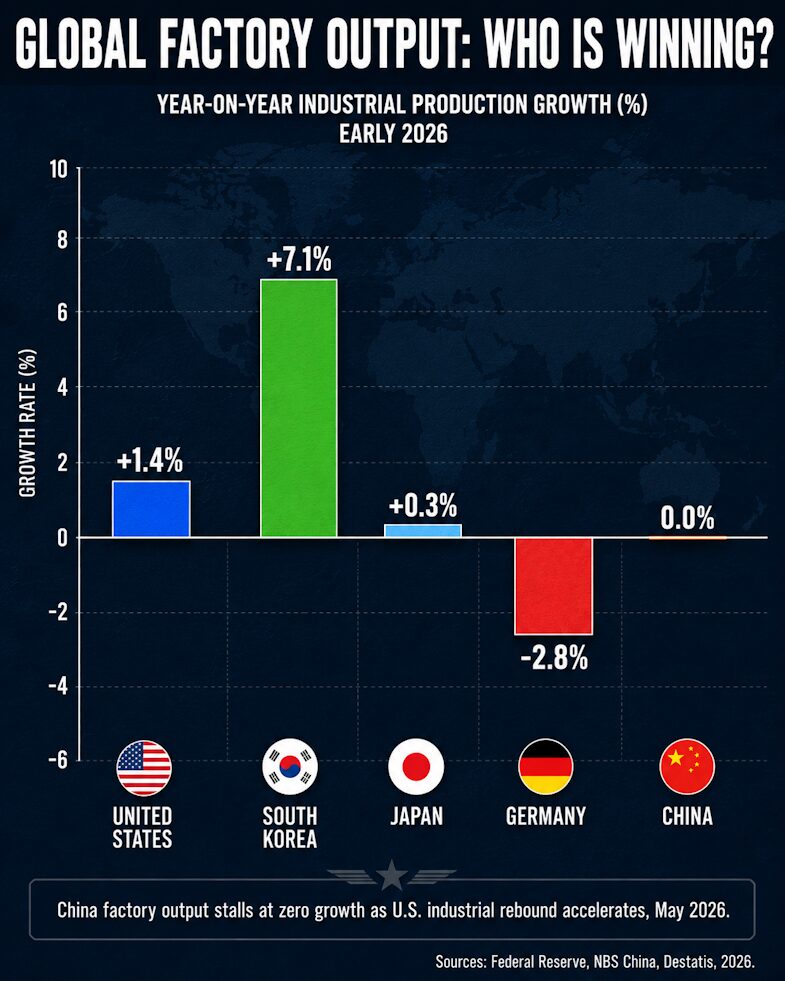

U.S. industrial rebound leads the world

While China factory output stalls and Germany contracts, the United States is moving in the opposite direction.

U.S. industrial output jumped 0.7% in April — much larger than expected — led by a 5.3% rebound in vehicle production.

U.S. manufacturing production has now grown on a year-on-year basis for fifteen straight months. High-tech industrial output rose 9.2% year over year in April alone.

This is the U.S. industrial rebound that the America First economic strategy was designed to produce — domestic manufacturing strengthening while competitor nations struggle with energy shocks and structural weaknesses they cannot quickly resolve.

The contrast could not be more stark.

China factory output flatlines. Germany shrinks. The U.S. industrial rebound accelerates.

South Korea is also performing strongly, with industrial production up 7.1% year-on-year in January 2026, driven by semiconductors, shipbuilding, and defense exports.

Japan posted modest but positive growth of 0.3% year-on-year.

The nations pulling ahead in 2026 share a common thread — they are investing in advanced technology, defense production, and AI-driven manufacturing rather than relying on cheap energy and cheap labor arbitrage.

That model is broken.

The U.S. industrial rebound is proof that a different model works.

War economies, AI manufacturing, and China’s arms quality problem

The wars in Ukraine and Iran have done something unexpected to global industrial production — they have created a massive, sustained demand shock for military hardware that is reshaping factory output worldwide.

Russia has enjoyed year-on-year manufacturing growth, driven almost entirely by war production.

Europe is rapidly militarizing in response to Russian aggression on NATO’s eastern flank — defense budgets are rising, ammunition production is being scaled, and countries like Poland, Romania, and the Baltic states are demanding hardware faster than Western defense industries can supply it.

Japan and South Korea are responding to the China threat in the Indo-Pacific with their own defense industrial expansion.

South Korea concentrates on scalable land systems and ammunition production while Japan specializes in advanced maritime systems, sensors, and missile technology.

This is a genuine industrial boom driven by geopolitical necessity.

China wants a piece of that boom — but cannot close the sale.

Chinese defense companies recorded a 10% decline in combined annual revenue in 2024, the lowest since 2009, even as total global arms exports reached $679,000 million.

International operators continue to report persistent reliability failures across Chinese military platforms — structural defects in fighter jets, catastrophic tank failures, and weak after-sales support.

China’s air defense systems exported to Iran performed poorly under real combat conditions during U.S. and Israeli operations, and an ongoing anti-corruption campaign has removed numerous senior defense executives tied to major state-owned contractors.

China factory output may be stalling — but China’s military export credibility is stalling even faster.

The world’s buyers are noticing. And the U.S. industrial rebound, combined with South Korea’s defense export surge, is filling the gap Beijing cannot.

The nations that invest in people, technology, and strategic clarity will win the industrial race of this decade. 🇺🇸 📊 ⚙️ #ChinaEconomy #AmericaFirst #Geopolitics

CMC, 1